Leopard Real Estate 2022 summary and market outlook

- Jan 19, 2023

- 11 min read

Leopard Real Estate Fund was launched in February 2022. The fund aims to achieve superior, long-term, risk-adjusted returns by investing in European-listed real estate companies. To achieve this goal, the fund targets companies that trade at a discount to their fair value, have sustainable cash flows, and have a track record of creating long-term value for shareholders.

In the beginning of 2022, the outlook for real estate companies was strong, due to optimism about reopening after the pandemic. However, by February, concerns about inflation and interest rate increases began to emerge. These concerns were exacerbated when Russia attacked Ukraine. The resulting high material and construction costs, rising interest rates, and concerns about leverage and refinancing all had a negative impact on the real estate market throughout the year. Despite this, many companies continued to see strong operational performance. However, the market for direct transactions became less liquid as the gap between buyers' and sellers' expectations grew. Yields in the residential and logistics markets were particularly hard hit in the second half of the year and this trend spread to all markets. By the end of the year, some companies began taking steps to address declining capital values, by cutting dividends, putting assets up for sale, or issuing new stock. However, more action will likely be needed as the market looks to recover in 2023.

As the world has transitioned from a period of Quantitative Easing to Quantitative Tightening, the fund increased its exposure to companies with lower leverage and higher dividend payouts while reducing exposure to companies with higher leverage. Despite these market conditions, the fund has performed comparably well and lost 25.6%, outperforming its benchmark, which has lost 34.8% over the same period, by 9.2%.

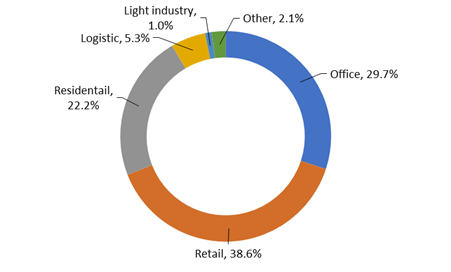

At the end of the year, the fund held a geographically diversified portfolio of high-yielding real estate companies. The weighted average dividend yield was 6.45%, and the weighted average discount to Net Asset Value stood at 41%.

During 2022, two of the fund's holdings were acquired by private equity, and I anticipate that this trend will continue in 2023, due to the fact that a large number of companies in the sector currently trade at valuations that suggest significant discounts compared to the market value of individual assets. While it is likely that asset valuations will decline in 2023, I believe that the companies the fund owns will perform better than the rest of the sector.

The increase in interest rates has both short-term and medium-to-long-term effects on real estate companies. In the short-term, companies that have financed with floating interest rates will experience a significant increase in their funding costs, leading to a decline in their earnings. The companies that have a significant portion of their financing fixed will have more time to adjust to the rising interest rates.

In the market, we see that companies are currently avoiding locking in interest rates at current elevated long-term rates, and are instead waiting for rates to settle. Additionally, many companies are switching from issuing public bonds to borrowing from traditional banks, which currently appear to offer more favorable terms.

In the fund's portfolio, we are focusing on companies that have a high percentage of fixed-interest debt with longer maturities, and on companies that own high-yielding properties that are better able to cope with elevated interest rates. Furthermore, we are specifically targeting companies that have a high degree of indexed leases, as these provide a degree of income protection in a rising interest rate environment.

Citycon

Citycon is a company that owns and manages urban shopping centers in the Nordic countries. It is a subsidiary of an Israeli-listed company and owns 35 assets that are typically located adjacent to major public transport hubs. Citycon's centers are anchored by grocery retailers and cater to daily necessities. The company's share price has been relatively resilient during 2022, declining by 10.5% while distributing a 7% dividend yield.

Citycon emerged from the Covid-19 pandemic in a relatively strong position, with Like-for-Like rents and rents per square meter higher than pre-pandemic levels. Occupancy stood at 95% as of year-end, and 92% of Citycon's rental income is indexed. Its rents on average make up a relatively low figure of 9% of tenants' revenue.

Like other real estate companies, Citycon's bonds are trading at elevated yields of 6-8%, which puts pressure on the company as it looks to refinance its public debt with banking partners, and sell assets that are considered to be non-core and of lower future potential. Citycon has earmarked €500 million of assets for sale, which will be used to deleverage and return capital to shareholders. The company does not have any significant debt maturities in 2023, and most of its debt has fixed interest rates.

As of the end of 2022, the company's share price implies that its real estate is worth 27% less than its book value, which means that the fund, as a shareholder, earns an attractive unleveraged yield of 6.3% on these Nordic assets.

G City, the parent company of Citycon, has been occupied in the last few years with restructuring its business. G City decided to exit Brazil and expand its development activities in the US, and also buy out the minorities in Atrium, a mall owner in Central Europe, and a subsidiary in which G City was the majority shareholder. The acquisition of Atrium served to increase the Net Asset Value of G City by buying out the minorities at less than book value and helped the share price of G City by eliminating the independent value assigned to Atrium’s assets by the market.

Pressure is growing on G City to reduce debt, and the company has been selling core and non-core assets to repay bonds. I believe, selling Citycon could be an option that is on the table and at the right price, the company could be acquired by investors that have a lower cost of capital than G City, which is currently trading at a distressed valuation.

Vonovia

Vonovia is the largest residential landlord in Germany, owning 550,000 apartments, 88% of which are located in Germany and the rest in Sweden and Austria. The German residential market is facing a long-standing shortage of investment in affordable rental housing, which has led to social unrest. Local governments have attempted to control rising rents, but some of these measures have been found unconstitutional by German courts. Meanwhile, factors like core inflation, a shortage of construction workers, and ongoing urbanization are continuing to drive up rents.

Like-for-Like rents across the Vonovia portfolio increased by 3% during 2022, and occupancy stood at a record high of 98%. This trend is expected to continue as there is no immediate solution to the shortage of supply, and it does not appear likely that the German government will have the resources, in the current European fiscal environment, to subsidize rents or the cost of acquiring a home. Further attempts to intervene in the market may also discourage investors and limit the supply of new build homes.

The company's share price dropped by 26% during 2022, and the company's various maturity bonds are trading at yields ranging from 3-5%. Vonovia is working to refinance its bonds and in October 2022 sold €1.5 billion of 4.75% and 5% yielding bonds. The company is also looking to sell properties to joint venture partners while continuing to manage them. Vonovia has approximately 10% of its liabilities coming due for refinance every year, with an average duration of 7.5 years and a current blended cost of 1.3%. Given the long maturity, I believe that inflation and the demand for housing should allow the company to continue and increase its Like-for-Like rents, to offset future higher refinancing rates.

CLS Holdings

CLS is a company that primarily owns office properties in secondary locations in the UK, Germany, and France. 25% of its tenants are government entities and 53% of its rental income is indexed. The company's management has created value for shareholders and earned a compounded annual return of 10% since 2000 through effective capital recycling and growing payouts to shareholders.

At the current share price, the implied price of the company's properties is approximately €2,000 and €2,900 per square meter for assets in Germany and France, and £340 per square foot for assets in the UK. This reflects a 33% discount on the book value of the properties and an unleveraged rental yield of 6.2%. I expect rental income to increase in the coming quarters as vacant space is refurbished and leased out.

In 2022, the company did a tender offer for its own shares, returning €30 million to shareholders. Management is currently committed to returning 50% of cash earnings as dividends, which currently yield 5%. The company has an average debt maturity of 4 years, with 80% of its debt fixed at a blended cost of 2.2% across the three geographies. I anticipate that the letting of vacant space, indexation in Europe, and rent reviews in the UK will allow rental income to keep pace with rising interest rates.

Patrimoine et Commerce

The company is a medium-sized retail landlord and owner of approximately 75 open retail parks across France. Occupancy across its portfolio has been stable during the pandemic and currently stands at 94%. Retail parks offer moderate occupancy costs for retailers and a lower pricing point for consumers, making them particularly attractive in times when inflation is affecting the profitability of companies and the budgets of consumers. Regulations on the development of new schemes have tightened the supply of new developments, and as a result, developers and owners have shifted their focus to refurbishing older stock rather than building new parks.

The company's current market value implies a low average cost of €1,200 per square meter for the company's assets and a net unleveraged yield of 6.7%. The current dividend yield stands at 8.3% while the Funds-From-Operations yield (which also includes cash profit not distributed) stands at 12%. The company's current debt cost averages less than 2%. Even if we model an immediate 2% interest rate increase across all the outstanding debt, we would still earn an FFO yield of 9% at the current share price.

Instone Real Estate

Instone is a developer of residential properties in Germany's top cities, with a history of selling most of its properties in the form of portfolios to institutional buyers. The company was listed on the German stock exchange in 2018 by its private equity sponsors.

According to the company's disclosures, 97% of its €2.7 billion projects currently under construction, have already been sold, and are expected to generate a cash flow of €600 million for the company. In addition, the company has approximately €440 million of land bank on its books. Offsetting this, the company has around €340 million of debt, resulting in shareholders' residual value of €700 million, compared to the current market value of €350 million, without considering the company's development platform that has generated margins of 25% in the past.

As interest rates increased in 2022, and the sale of condominiums and portfolios slowed down, the company's share price dropped by 51%, causing its previous private equity sponsors to acquire 27% of the outstanding shares. In addition, the company completed a share buyback of €25 million in 2022 (5% of shares outstanding) and approved the purchase of an additional 2.9% until March 2023.

The company's debt is mostly fixed at 4%, and its next material debt maturity is in 2025. I believe that the market has overreacted and punished the company's share price more than is appropriate. The company is trading at a discount to the future cash flow from the pipeline of sold projects and the value of its land bank. Furthermore, no value is assigned to the potential of the land bank to generate profits. Germany lacks affordable and sustainable housing, and the number of urban households is growing as a result of immigration, urbanization, and a reduction in the average size of households. Therefore, I believe that Instone will continue to generate significant profits once interest rates stabilize, as housing is in short supply and buyers adjust for higher rates.

Workspace

Workspace is a leading provider of flexible office space in London, owning 64 properties across 500,000 square meters, primarily leased to small and medium-sized businesses. The company's tenants sign a two-year lease with a 6-month rolling break option, but on average, they stay for a period of 5 years. The company's assets are well-located and 68% of the space is in the process of or has already been, rated Energy Performance Certificate (EPC) A-C, ahead of a 2025 imposed deadline.

The company's share price declined by 45% during 2022, and the current valuation implies a value of approximately £400 per square foot, which is a significant discount to London office space prices. The company's occupancy at its stabilized locations is back to 90%, similar to its pre-Covid level. I believe the company's product will continue to be in high demand as tenants are turning to more hybrid working models and are inclined to commit to a long-term lease. Furthermore, reaching 90% occupancy gives the company a comfortable position from which to increase rent for its new and current tenants.

Going forward, the company will focus on refurbishing older stock and selling non-core assets acquired during 2022 as part of an M&A transaction. The proceeds will be used to reduce acquisition financing, while the refurbished properties will add top-line growth. The current dividend yield of 5% should be resilient to the increased interest rates due to the company's low leverage combined with top-line growth in rental income.

Intervest Offices & Warehouses

Intervest is a recent addition to the fund's portfolio. The company owns a portfolio of mostly logistics properties located in Belgium and the Netherlands, with the rest of the assets being office buildings. Belgium and the Netherlands serve as gateway countries into Europe through the ports of Rotterdam and Antwerp, the two largest ports in Europe. Intervest has been growing internally through its own property development and through accretive acquisitions of leased properties. The company's sustainable logistics portfolio has no vacancy, and the company is developing an additional 400,000 square meters of modern logistics rental space. 32% of the portfolio's assets have already achieved a green certificate of at least "Very Good" and 89% of the logistics assets have solar photovoltaic systems installed.

The company's leases are index-linked, providing the company with strong protection against rising interest rates, which currently stand at 1.8%. After dropping 32% in 2022, the current share price implies an unleveraged rental yield of 7% and a leveraged return of 9.5% (excluding the non-producing properties in the development phase). The high-yield return, rent indexation, and further development potential provide a reasonable margin of safety against a future rise in the cost of the company's debt.

Palace Capital

The small-cap landlord owns a diversified portfolio of office, leisure, logistics, industrial and residential properties across the UK. In July the company announced its intention to sell the industrial portfolio and invest the proceeds into energetic upgrades of its non-ESG-compliant properties and the acquisition of additional ESG-compliant properties. However, following discussions with shareholders, the company announced a strategy shift and that it will focus instead on maximizing cash returns to shareholders. It seems management is looking to sell all the properties of the company or the company as a going concern, once the pricing of real estate has stabilized.

During 2022, the share price of the company dropped by 19%, while distributing a 6% dividend yield. Although the company has a low level of debt, its current share price implies a steep discount to its book value of 32% and a hefty 10% rent yield. I believe that the break-up value of the company is probably about 40% higher than where the shares currently trade.

Befimmo

The fund acquired shares of Befimmo, a Belgian and Luxembourg-focused office Real Estate Investment Trust (REIT), soon after its launch in February. Later that same month, Brookfield, a major real estate private equity investor, made a tender offer to purchase the shares of the REIT at a price of 47.5 Euro, which represented a premium of over 50% on the market value at the time. Despite this premium, the offer still reflected a discount of more than 20% on Befimmo's Net Asset Value. The fund invested in Befimmo due to its attractive 6% dividend, low leverage and development pipeline.

Deutsche Euroshop

Deutsche Euroshop, the largest owner of malls in Germany, received an offer in May from a joint venture formed by its largest shareholder and Oaktree, a private equity firm. The share price of the company had been suppressed by the impact of Covid, but I believed that the Covid effect was temporary and that the company would reinstate its dividend. At the time of acquisition, our cost base suggested an unleveraged return of 7.5%, which was significantly higher than the yield available on similar stand-alone assets. The fund had accumulated shares in the company since its launch in February and sold the position with a 30% profit in May.